Advertisement

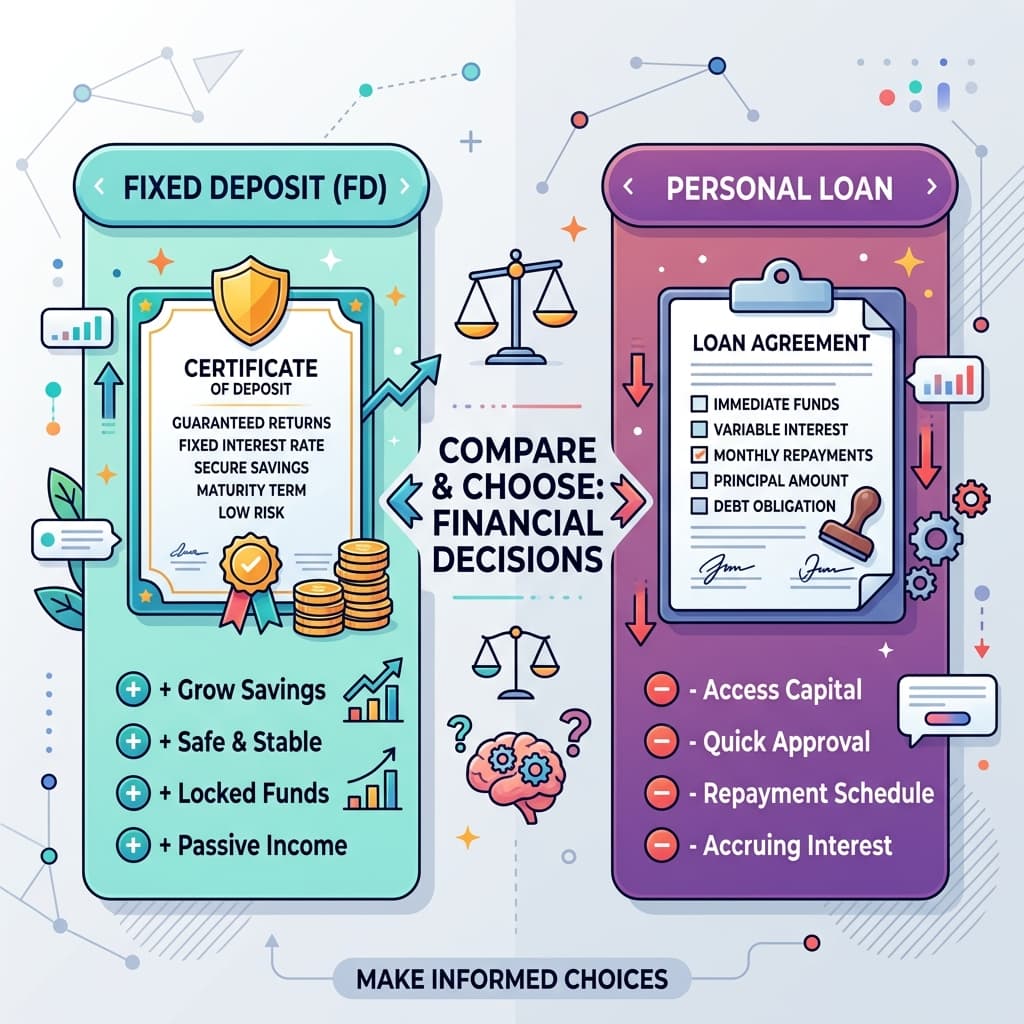

Imagine you have a ₹5 Lakh Fixed Deposit (FD) maturing in two years, earning 7% interest. Suddenly, a medical emergency strikes, and you need ₹3 Lakhs immediately.

You have three options:

- Break the FD prematurely.

- Take an unsecured Personal Loan for ₹3 Lakhs.

- Take a Loan Against your FD (an Overdraft facility).

While breaking the FD is usually the default reaction, it triggers a premature withdrawal penalty (typically 1%) and you lose all future interest. The real debate usually boils down to a Personal Loan versus a Loan Against FD.

Which is the smarter financial move?

Key Takeaways

- Interest Rates: A Loan Against FD is extremely cheap. The bank only charges 1% to 2% above your FD rate. Personal loans cost between 11% to 18%.

- No CIBIL Required: Since the loan is fully secured by your own money, banks do not require income proofs, salary slips, or a high CIBIL score for a Loan Against FD.

- Overdraft Flexibility: A Loan Against FD acts as an overdraft limit. You only pay interest on the amount you actually use, for the exact number of days you use it.

1. What is a Loan Against FD?

A Loan Against FD (also known as an Overdraft against FD) allows you to pledge your existing Fixed Deposit as collateral to the bank in exchange for a credit line.

Typically, banks will give you a credit limit of 85% to 90% of your FD value. If your FD is worth ₹5 Lakhs, the bank instantly opens an overdraft account linked to it with a limit of ₹4.5 Lakhs.

The Pricing Rule

The interest rate on a Loan Against FD is pegged directly to the FD's earning rate. Most banks charge exactly 1% to 2% higher than what the FD is earning.

- If your FD earns 7% p.a.

- The Loan Against FD will cost you 8% to 9% p.a.

2. Personal Loan vs Loan Against FD: Head-to-Head

Interest Rates

- Personal Loan: 11% to 18% (depending on your credit score and employer).

- Loan Against FD: 8% to 9% (usually just 1% to 2% above your FD rate).

Processing Fees

- Personal Loan: Banks typically charge a 1% to 3% processing fee plus GST. On a ₹3 Lakh loan, this is ₹3,500 to ₹10,000 down the drain.

- Loan Against FD: Zero processing fees in most major banks.

Repayment Flexibility

- Personal Loan: Rigid monthly EMIs. If you suddenly get a bonus and want to close the personal loan early, banks slap a 3% to 5% foreclosure penalty on you.

- Loan Against FD: Ultimate flexibility. It functions like a credit card limit. You only pay interest on the exact amount you withdraw. If you deposit money back into the account the next week, the interest meter stops. There are zero foreclosure charges.

To calculate exactly how much money you save by choosing the lower interest rate, use our Loan Comparison Tool:

Practical Example: Borrowing Your Own Money

You have a ₹5 Lakh Fixed Deposit earning 7% interest. You suddenly need ₹3 Lakhs for a home renovation.

- Mistake (Personal Loan): You apply for an unsecured Personal Loan. The bank charges you 15% interest and a ₹5,000 processing fee. You are losing money fast.

- Smart Move (Loan Against FD): You ask the bank for an overdraft against your FD. They instantly give you ₹3 Lakhs without paperwork. The interest rate is strictly 2% higher than your FD rate (i.e., 9%). You continue to earn 7% on your FD, so your net cost of borrowing is effectively just 2%.

3. When Does a Personal Loan Make Sense?

Given how cheap and flexible a Loan Against FD is, why would anyone take a personal loan?

- You Don't Have an FD: The most obvious reason. You cannot take a Loan Against FD if you don't have a large enough deposit to pledge.

- You Need More Than 90%: If you need ₹10 Lakhs, but your FD is only worth ₹5 Lakhs, the bank will only give you a limit of ₹4.5 Lakhs. A personal loan can be granted for much higher amounts based on your salary multiplier.

4. The "Breaking the FD" Alternative

What if you just break the FD? If you break a ₹5 Lakh FD halfway through its tenure, the bank will calculate the interest for the period it actually ran, minus a 1% penalty.

Rule of Thumb:

- If you need the money for a very short period (e.g., 3 months) and you expect a cash inflow soon to pay it back, take the Loan Against FD. The 1% extra interest for 3 months is cheaper than the 1% penalty on the entire FD principal.

- If you need the money permanently and have no cash flow to repay the loan, break the FD. There is no point paying 9% interest to the bank when you have no means to repay it.

To see the math behind breaking an FD prematurely, use our Premature FD Penalty Calculator:

Action Steps

- Check Your Net Banking: Most banks (SBI, HDFC, ICICI) allow you to open a Loan Against FD instantly via net banking with a single click. No paperwork or branch visit is required.

- Never Pay Personal Loan Fees: If you must take a personal loan, negotiate the processing fees down to a flat ₹999 or zero.

Related Reading

- Fixed Deposit vs Recurring Deposit , Which One Should You Choose?

- Personal Loan vs Credit Card: Which Debt is Cheaper?

- DICGC Insurance , Is Your Bank Deposit Really Safe?

Frequently Asked Questions (FAQs)

What is the core concept behind loan against fd vs personal loan a complete comparison?

Need cash but don't want to break your Fixed Deposit? We compare taking a Loan Against FD versus an unsecured Personal Loan to find the cheapest borrowing option.

Can you explain: 1. What is a Loan Against FD??

A Loan Against FD (also known as an Overdraft against FD) allows you to pledge your existing Fixed Deposit as collateral to the bank in exchange for a credit line..

Can you explain: 2. Personal Loan vs Loan Against FD: Head-to-Head?

- Personal Loan: 11% to 18% (depending on your credit score and employer)..

Grow Your Service Business Online

Spend less time managing appointments and more time growing your business. Accept appointments 24/7, manage walk-ins, schedule staff, and track revenue from one place.

Put this into practice

Use our free interactive calculators to plan every aspect of your finances.

Table of Contents

- 1. What is a Loan Against FD?

- The Pricing Rule

- 2. Personal Loan vs Loan Against FD: Head-to-Head

- Interest Rates

- Processing Fees

- Repayment Flexibility

- Practical Example: Borrowing Your Own Money

- 3. When Does a Personal Loan Make Sense?

- 4. The "Breaking the FD" Alternative

- Action Steps

- Related Reading

- Frequently Asked Questions (FAQs)

Myat Finance Editorial Team

Financial EducatorsThe Myat Finance editorial team consists of dedicated financial analysts, developers, and educators. Our mission is to make personal finance in India transparent, mathematical, and free from mis-selling. We build data-driven tools and write unbiased guides to help you make smarter money decisions.

Compare Top Loan Offers

Disclosure:These are unbiased affiliate links. We may earn a commission if you open an account, at no extra cost to you. We recommend comparing platforms and selecting the one that best fits your financial needs.

You May Also Like

More articles about Loans & Debt Management

Home Loan EMI on ₹40 Lakh: The Complete Breakdown

Personal Loan vs Car Loan: Which is Actually Cheaper?

How to Get Out of a Debt Trap: A Step-by-Step Recovery Plan

Was this article helpful?

Master Your Money, Weekly.

Join 10,000+ Indians receiving our best wealth-building strategies, tax loopholes, and financial tool updates every Sunday. No spam, just value.

We respect your inbox. Unsubscribe anytime.